A brand-new start-up intends to assist you get your trainee loans under control. Today, an app called Pillar , backed by $5.5 million in seed financing led by Kleiner Perkins, is introducing an easier method for customers to much better comprehend their trainee loan financial obligation and even pay it off early.

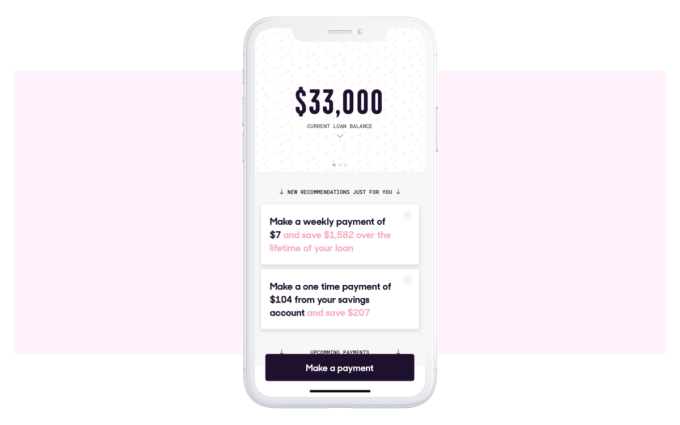

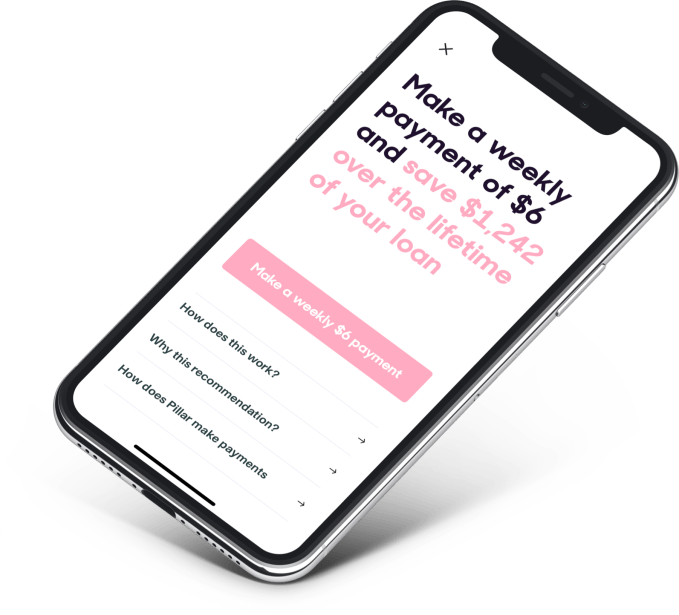

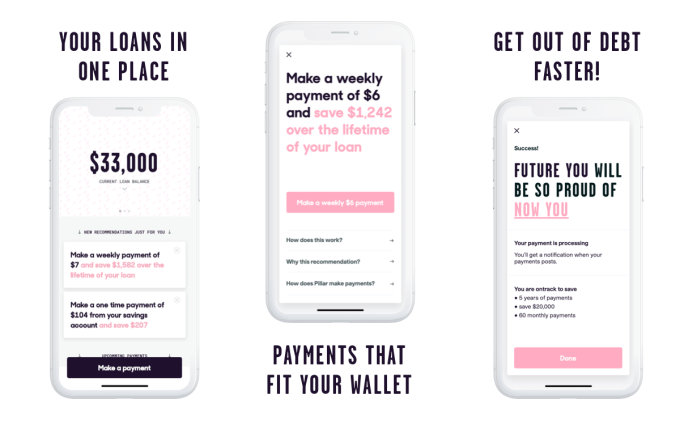

To do so, the app gets in touch with your trainee loan servicer and bank, then makes individualized tips based upon your loans, your earnings and your costs. It will send out an alert to your smart device when it discovers a method you can make a larger damage in your total trainee loan financial obligation.

Pillar co-founder and CEO Michael Bloch, an early DoorDash staff member, stated he created the concept after his better half finished from law school with around $300,000 worth of trainee loans.

“We had a hard time to find out properly to pay them back,” he describes. “We check out post and short articles. We made spreadsheets. We even talked with a monetary consultant. There truly was no simple method for us to figure out what was the ideal thing for us to do. And I understood there are 45 million individuals with loans, and countless those individuals have actually had the precise very same experience as I did.”

Bloch chose then to leave of Stanford Business School to rather concentrate on structure Pillar together with co-founder and CTO Gilad Kahala.

Above: Michael Bloch (L) and Gilad Kahala (R)

The issue they’re assaulting is enormous. Trainee loan financial obligation is the 2nd biggest kind of customer financial obligation in the U.S., with 45 million customers owing more than $1.5 trillion in trainee loans. 7 out of 10 trainees secure loans to spend for college, and the typical individual graduates with $30,000 in financial obligation, which takes 20 years to settle. For those with $60,000 in financial obligation, it can take more than 30 years to settle. And almost 20% of customers have more than $100,000 in financial obligation.

In addition, ladies are disproportionately impacted by this issue, keeps in mind Bloch. Females hold two-thirds of trainee loan financial obligation, he explains. This is since there are more females (around 56%) than guys going to college nowadays, and due to the fact that of the gender pay space which indicates it takes longer for ladies to repay their loans.

At launch, Pillar strolls brand-new users through a fast sign-up procedure where you confirm with your loan service provider and savings account. (The business states it utilizes security best practices, and does not save any login info or passwords by itself servers.)

As Pillar examines your costs and pay schedule, it can determine when you can begin making an additional payment towards your loans. It likewise computes what that implies in regards to settling your loan previously. This is specifically helpful for those who do not always get a consistent income, or whose earnings changes for other factors they might have problem figuring out just how much they can really pay for to chip in.

The business does not provide to re-finance loans, to be clear, nor will it point you towards those alternatives. It anticipates numerous of its users would not be able to take benefit of re-financing choices, anyhow.

“Companies like SoFi in fact turn away around 97% of everyone who requests refinancing, due to the fact that they’re too expensive a credit threat they take a look at your credit history, your earnings, the kind of task you have the majority of people do not receive lower rates on refinancing,” Bloch states.

Instead, Pillar targets the bigger bulk who earn less than $100,000 annually and have less alternatives.

“What we discovered is that these little actions that individuals can take where it’s not always a hundred dollars this month. Even making a $5 a week additional payment can make an actually huge distinction to someone’s monetary life in the long run,” he describes.

Users can decide to make these extra payments through Pillar itself, rather of needing to go through the often cumbersome trainee loan service provider’s site.

Pillar deals with almost all significant trainee loan servicers consisting of Nelnet, Navient, Great Lakes, Fedloan Servicing and others.

Prior to today, the business had actually been running a personal beta with a concealed variety of users who are now utilizing Pillar to handle their cumulative $50 million-plus in loan financial obligation. Throughout this duration, the typical debtor conserved around $6,000 and about 4 years on payment, Bloch claims.

What Pillar does refrain from doing, at this moment, is assistance customers browse trainee loan forgiveness programs. That’s on its roadmap. It prepares to provide tools and automation to assist its users browse those programs in the future. Longer-term, Pillar wishes to provide for all customer financial obligation consisting of charge card what it’s now providing for trainee loans.

While Pillar is assaulting a genuine issue, it’s not yet a detailed option and even the very best method for a customer to manage their general financial obligation.

As Genevieve Dobson, creator and CEO of financial obligation management business Degrees of Success , points out, the interest rates on customers’ trainee loans might be lower than the high interest rates on their credit cards and other financial obligation that need to be paid down.

Plus, she keeps in mind, “it would not be recommended for anybody who gets approved for an income-based payment or other lower payment alternative. It’s likewise not an excellent alternative for those who receive any of the forgiveness programs. And regrettably, it does not appear to inform individuals to use the income-driven payment alternatives rather, which might wind up damaging somebody instead of assisting them.”

In time, ideally, Pillar will end up being more thorough to attend to the requirements of all debtors. In the meantime, nevertheless, it makes the very best sense for those who just hold trainee loan financial obligation and are aiming to pay it down quicker.

Pillar states it will keep all its guidance complimentary, however will charge a low (around $1 monthly) membership cost for premium functions at some time in the future. The business will likewise offer (not offer) anonymized loan information to nonprofits and research study organizations who are working to advance the nationwide discussion and policy around trainee loans.

In addition to Kleiner Perkins, other seed round individuals consist of Rainfall Ventures, Great Oaks VC, Financial Venture Studio, Kairos and Day One Ventures. Specific financiers consist of Adam Nash, the previous CEO of Wealthfront and Acorns board member; Noah Weiss, previous SVP of Product at Foursquare; Zach Weinberg and Nat Turner, co-founders of Flatiron Health; Misha Esipov, CEO and co-founder of Nova Credit; and Robinhood’ s head of International, Patrick Kavanagh, and head of Finance, Nadia Asoyan.

The Pillar group is presently 10 individuals in New York, and aiming to double the size of the group over the next year with a specific concentrate on working with engineers.

Pillar is offered on iOS and Android . You will still require to sign up with the waitlist, as individuals are being permitted into Pillar in phases as it releases.

Recent Comments